Economic growth is an increase in the production and consumption of goods and services. For distinct economic or political units, economic growth is generally indicated by increasing gross domestic product (GDP). Economic growth entails increasing population times per capita consumption, higher throughput of materials and energy, and a growing ecological footprint. Economic growth is distinguished from “economic development,” which refers to qualitative change independent of quantitative growth. For example, economic development may refer to the attainment of a more equitable distribution of wealth, or a sectoral readjustment reflecting the evolution of consumer preference or newer technology.

The size of an economy may undergo one of two trends: growth or recession. Otherwise it is stable, in which case it is a “steady state economy.” As with many phrases, however, different connotations may apply in different contexts. In neoclassical economics, the hyphenated phrase “steady-state economy” is used to refer to an economy with steady ratios of capital:labor. Therefore, in neoclassical economics, a steady-state economy may be growing, receding, or stable, in which case it constitutes the steady state economy of ecological economics. Sometimes, however, the hyphenated “steady-state economy” is also used in the ecologically economic sense of a non-growing, non-receding economy. (In some cases this reflects the editorial style and tradition of a particular journal.) This linguistic inconsistency is not a major communications problem in broad circles because the neoclassical “steady-state economy” is a relatively abstruse concept used primarily within the jargon of neoclassical economics, whereas the ecological “steady state economy” is a technically simpler concept and has achieved a certain amount of vernacular status.

Yet regarding linguistics, the issue of hyphenation has some import. It is appropriate to use the unhyphenated phrase “steady state economy” to describe an economy of stable size because “state” (as in political state) is an adjective of “economy” (as in a state’s economy), and “steady” is an adjective of this state economy. In other words, “steady state economy” typically refers to a national economy of stable size, although it may also refer to an economy of a city, province, or other political unit. (It may also refer to a regional economy or the global economy, and in such cases political units are aggregated.) In neoclassical economics, “steady” is not an adjective of “state economy.” Rather, the conjoined “steady-state” is a heuristic tool to imply the stable ratio of capital:labor and, linguistically, is an adjective of “economy.”

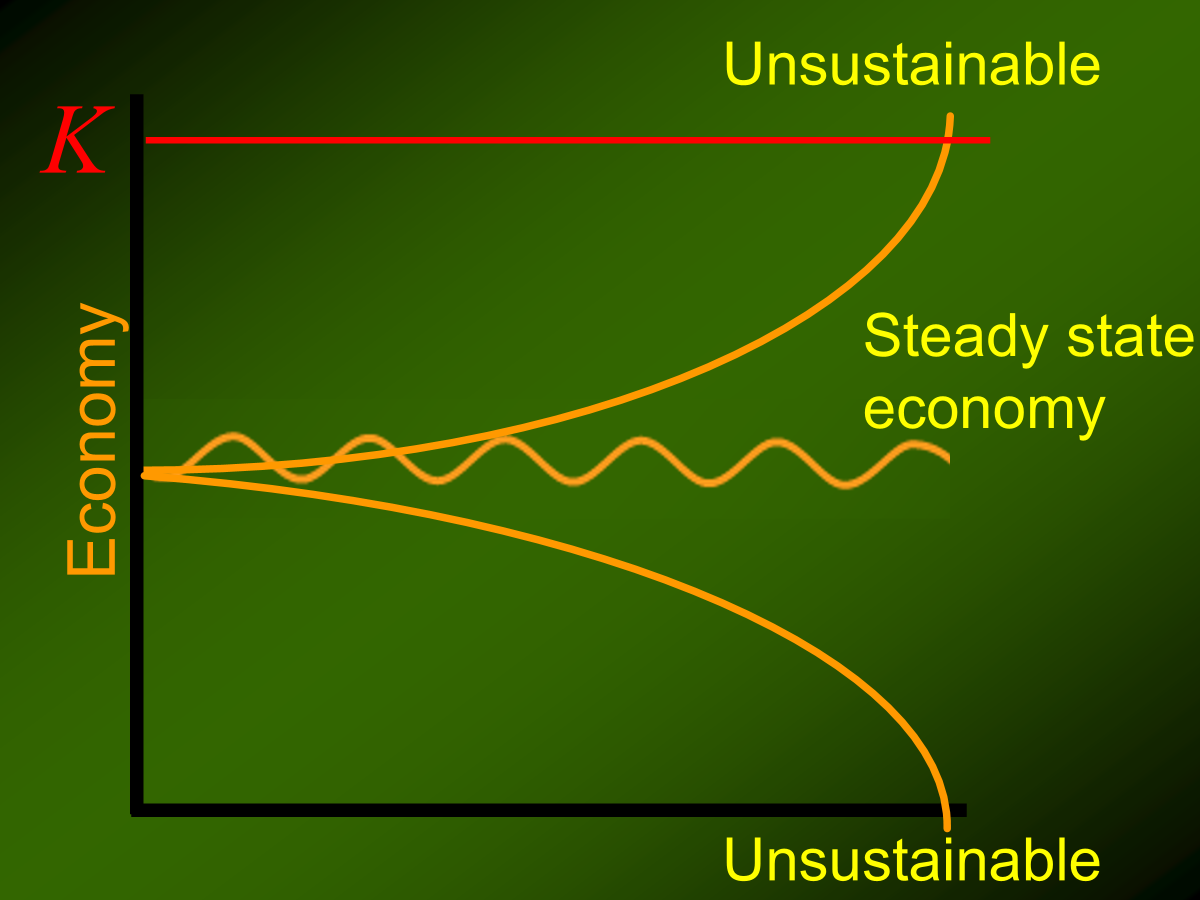

Theoretically and temporarily, a steady state economy may have a growing population with declining per capita consumption, or vice versa, but neither of these scenarios are sustainable in the long run. Therefore, “steady state economy” connotes constant populations of people (and, therefore, “stocks” of labor) and constant stocks of capital. It also has a constant rate of throughput; i.e., energy and materials used to produce goods and services.

Within a given technological framework these constant stocks will yield constant flows of goods and services. Technological progress may yield a more efficient “digestion” of throughput, resulting in the production of more (or more highly valued) goods and services. However, as emphasized in biophysical economics (which may arguably be classified as a subset of ecological economics), there are limits to productive efficiency imposed by the laws of thermodynamics and therefore limits to the amount and value of goods and services that may be produced in a given ecosystem. In other words, there is a maximum size at which a steady state economy may exist. Conflicts with ecological integrity and environmental protection occur long before a steady state economy is maximized.

“Constancy” of population and capital stocks does not imply absolutely unchanging population and capital stocks at the finest level of measurement. Rather, “constant” implies mildly fluctuating in the short run but exhibiting a stable equilibrium in the long run. Long-run changes reflect evolutionary, geological, or astronomical processes that alter the carrying capacity of the Earth for the human economy. Dramatic examples include atmosphere-altering volcanoes and massive meteorite collisions.

Just as economic growth is the predominant macroeconomic policy goal identified or implied by neoclassical economics, the steady state economy is the predominant macroeconomic policy goal identified or implied by ecological economics. To the extent that ecological economics is a normative transdisciplinary endeavor rather than a purely analytical framework, its three main concerns are sustainability, equity, and efficiency, each of which may be served via public policy. Neither economic growth nor economic recession are sustainable; therefore, the steady state economy remains the only sustainable prospect and the appropriate policy goal for the sake of sustainability.

The steady state economy may be pursued in the policy arena with the same policy tools that have historically been used to facilitate economic growth. These include fiscal policy tools such as government spending and taxation, and monetary policy tools such as money supplies and interest rates. Certain institutional adjustments are also entailed. For example, some have posited that a fractional reserve banking system may not be reconciled with a steady state economy and that fee-service banking is the most feasible alternative. Other public policies pertaining to ecological integrity and environmental protection may also be conducive to a steady state economy. For example, some have posited that the Endangered Species Act of 1973 was an implicit prescription for a steady state economy balanced with an economy of nature characterized by numerous threatened and endangered yet stabilized species.

Further Reading