Special Report: Introducing the Sustainable Monetary Policy Act

by Brian Czech

The Marriner S. Eccles building in Washington, DC, home of the Federal Reserve Board of Governors. (Jbarta, CC BY-SA 3.0)

The Federal Reserve System has more influence over the rate of economic growth—certainly nationally and arguably globally—than any other institution. When it sets the federal funds rate, the Fed affects the decisions of producers and consumers far and wide. When it lowers the rate, producers borrow more, from Midwest farmers to Silicon Valley techs. Likewise, consumers borrow more for everything from cars and houses to laptops and smartphones. People roll their sleeves up, the economy is stimulated, and GDP grows.

At least, that’s what the Fed hopes. At times, though, the Fed finds itself “pushing on a string,” dropping the federal funds rate with little effect on economic activity. But the Fed has numerous tools and tactics for stimulating economic activity, and it has a long track record of doing so.

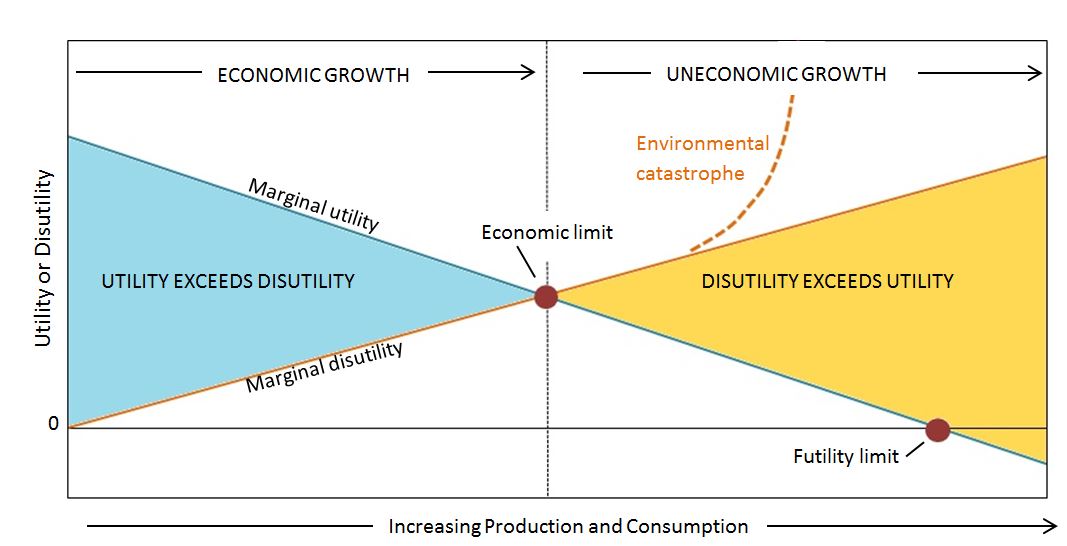

That was a good thing for much of the 20th century, but it was bad for the environment. By the latter decades of the century, the global economy was clearly in ecological overshoot. This realization, stemming from fuller integration of the natural sciences, gradually spawned the poorly funded but conceptually powerful field of ecological economics. Today, the calls to look “beyond GDP” are going mainstream, and they’re not just about the GDP metric. They’re a diplomatic way of saying that economic growth—increasing production and consumption of goods and services in the aggregate—is no longer a suitable goal for the world, all things considered.

Meanwhile, growth remains ingrained in Fed culture, given the Fed’s deep ties to Wall Street. Its governors are typically economists or lawyers, many of whom move in and out of the private banking sector, Fortune 500 corporations, government, politics, and academia. Among its professional staff, the Fed employs over 400 Ph.D. economists, practicing a profession notorious for the “invention of infinite growth.”

Beyond its culture, the Fed is mandated, pursuant to the Federal Reserve Act amendments of 1977, to proactively promulgate economic growth. In particular, it must “maintain long run growth of the monetary and credit aggregates…so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

Strictly speaking, then, growth per se is not the goal, but rather a means to achieve “maximum employment.” The logic is straightforward. All else equal, a growing GDP entails an increasing number of jobs. That’s especially important when a population is growing at a significant rate.

If the real economy is growing, with more jobs and all, “growth of the monetary and credit aggregates” (a growing money supply, especially) is needed for “stable prices.” Incidentally and conversely, growing the money supply is conducive to a growing real economy, at least in the short term.

But with those 1977 amendments, Congress was trying to have its cake and eat it too. By then, the Phillips curve, demonstrating the inverse relationship between unemployment and inflation, had been circulating for almost 20 years. Lowering the federal funds rate was growthmanship 101, but it was (and is) inflationary. Readjusting the rate upward helps stabilize prices, but it’s recessionary.

The “dual mandate” of the Fed turned out to be mission impossible, and the source of tremendous political and financial strain. But there’s a simple cure: the steady state economy. This will surely take an act of Congress, prefaced as follows.

Mission Possible, and Proper for the 21st Century

Unfortunately, the steady state economy is a cure that the Fed, as currently cultured, is bound to reject. At best, the Fed might view it as one part cure and two parts poison. Led by Kevin Warsh, the anti-regulation, pro-growth Chair, the Fed would likely be one of the last bastions of growthmanship, even if the rest of the polity moved toward steady statesmanship.

The Fed’s dual mandate was less impossible—and less destructive—when Mission Impossible aired in the 1960s. (Banknotes meant more, too.) (Wikimedia Commons, Public Domain)

So it’s a waiting game for the logic to seep into the Fed that the best way out of the dual-mandate dilemma is to abandon the goal of growth and adopt the goal of a steady state economy. The logic should be seeping in soon, given that the U.S. population has nearly stabilized. That makes the goal of full employment more achievable without a growing GDP. It also makes achieving (or even “promoting”) economic growth a losing battle.

The population is projected to fully stabilize around 2056, opening a wide and obvious window for “steady statesmanship” in monetary policy. Given that the steady state economy amounts to stabilized population × per capita consumption, the steady state economy will be halfway established, in a sense, as the century reaches the halfway mark.

However, the Fed is so steeped in the growth paradigm that it is likely, even in the context of a stable population with full employment, to interpret its mandate as a call for economic growth per se. The growth would be deemed desirable not so much for the purpose of maintaining full employment—a goal already accomplished—but for the further purposes of increasing per capita consumption and GDP. To defend that interpretation, it will no doubt point to the Full Employment and Balanced Growth Act of 1978, a sort of twin jet to the 1977 Federal Reserve Act amendments.

For the Fed to accept the logic of a steady state economy being congruent with its mandate, then or ever, it will have to develop some expertise in ecological economics. Otherwise it will remain oblivious to ecological limits and the environmental costs of growth. Even if it becomes more aware of biodiversity loss, climate change, and the unravelling of the planetary ecosystem, the Fed will fall back on the old fuzzy notion that technological progress will resolve any conflicts between economic growth and environmental protection.

The Fed will overlook the fact that research and development (the process of technological progress) entails economic growth based upon pre-existing levels of technology. It will ignore the fact that such growth will be causing the very environmental deterioration that the technological progress will be expected to mitigate from behind the 8-ball. It will overestimate the availability of environmentally beneficial R&D funding, conveniently forgetting about the numerous other forces in the private and public sectors competing for profits, dividends, and economic surplus in general.

In other words, it will take a Sustainable Monetary Policy Act to foist some ecological economics into Fed leadership and staff. A section on reorganization, at a minimum, can help with this challenge.

To inject a bit of good news, though, consider the heights to which the Fed could bring the field and practice of ecological macroeconomics, if only it chose to dig in and do so. What staunch and effective steady staters they could be!

Opening Eyes and Minds to Ecological Limits

It’s not only the Fed that has a difficult time spotting or accepting limits to growth. So did William Greider, the deep-diving author who divined the Secrets of the Temple (his dramatic handle for the Fed). At the 711th page of his exhaustive analysis, Greider produced this telling paragraph:

“From the sixties onward, each succeeding decade produced slower growth, higher levels of permanent unemployment and declining real wages, less progress on capital formation and productivity. For many years, all these portentous developments had been blamed on inflation. Now that inflation was gone [1986], it was obvious that something else was responsible, deeper problems in the aging economic structure that remained unattended.”

Ecological economics is a poorly funded, yet richly conceptualized framework to help the Fed in determining the “monetary and credit aggregates” central to its mandate. (Issuu)

Yes, it certainly was obvious that something else was responsible, but for ecological economists, so was the “something else.” Limits to growth. Environmental, ecological, and therefore economic limits. By these later decades of the 20th century, the low-hanging thermodynamic fruits had been picked. It was getting more difficult by the year to find the land and resources—the “natural capital”—required to adequately complement the outsized stocks of labor and capital (manufactured and financial) for the sake of vigorous economic production.

Yet in the entirety of Greider’s 798-page tome, the environment never showed up. Nothing about limits to growth, the Club of Rome, Herman Daly, steady-state economics… all of which were in play during Greider’s project.

It’s not so much a critique of Greider; Secrets was more or less a biography of the Fed, not an interdisciplinary treatise. And, of the gazillion meetings attended by Fed Chair Paul Volcker and duly reported by Greider, there didn’t seem to be a single one with the Secretary of the Interior, Secretary of Agriculture, EPA Administrator or any other leader with (we would hope) a good grasp of ecological limits.

A similar phenomenon was revealed in Lords of Easy Money by the top-notch investigative journalist Christopher Leonard. To wit, from page 302:

“[Fed Governor Tom] Hoenig’s warnings in 2020 were different in one important way from his warnings a decade earlier. Now he could point to the historical record… In the 1990s labor productivity in the United states increased at an annual rate of 2.3 percent. During the decade of ZIRP [zero interest rate policy], it rose by only 1.1 percent… Average real GDP growth, a measure of the overall economy, rose an average of 3.8 percent annually during the 1990s, but by only 2.3 percent during the recent decade. The only part of the economy that seemed to benefit under ZIRP was the market for assets. The stock market more than doubled in value during the 20 tens. Even after the crash of 2020, the markets continued their stellar growth and returns.”

In other words, while the Fed was pulling out all the stops with unheard-of zero percent interest rates (and other desperate measures), the economy just wouldn’t grow as it had decades prior. Not the real economy as measured with GDP. Limits to growth were kicking further in, so instead of making a dent in the real economy, the vast majority of stimulus money flowed into Wall Street, stirring speculators into action and inflating asset prices. “Fictional capital,” some call it (echoing Marx’s concept of “fictitious capital”).

Leonard also quoted Ben Bernanke himself: “But the fact is that nobody really knows precisely what is holding back the economy” (page 140). And, like Greider, Leonard never mentioned the environment in the 373 pages of Lords.

Nor did insiders Danielle DiMartino Booth and Joseph Wang, who wrote Fed Up and Central Banking 101, respectively.

The Fed book with the most promising title—Limitless: The Federal Reserve Takes on a New Age of Crisis by Jeanna Smialek—had nothing explicit about limits to growth. However, it did include some anecdotes about an interest in climate change taken by some Fed principals, including Lael Brainerd and Jerome Powell. There’s a seed of hope in that. In general, though, Smialek described a Fed that is light years behind its cousins in the central banking community (much less the sustainability sciences) when it comes to the big-picture, long-term concern of climate change. And so far, even among the European central banking cousins, it’s more about “green growth” than limits thereto.

You can’t really blame these authors. They were mostly trying to describe what the Fed did and does. They just never witnessed Fed principals discussing limits to growth, ecological macroeconomics, or even the basic environmental underpinnings of the economy. Certainly not enough to warrant any reporting thereon.

In the Sustainable Monetary Policy Act, Congress must find and declare limits to growth, loud and clear, providing guidance to the Fed for learning and applying such crucial knowledge. The Fed needs this knowledge, not only for helping to manage a sustainable economy, but so they can stop beating their heads against the wall with the likes of ZIRP, QE, and SPVs (“special purpose vehicles,” yet another mechanism for increasing liquidity).

Utilizing a New Capacity

It’s not that the Fed has no concept of capacity. They clearly do, as evidenced by their “capacity utilization” data. The problem is that the Fed limits the concept to manufacturing, mining, and electric and gas utilities. And there is scant evidence that the Fed has a good grasp of the natural resources involved in production. Production functions, taught to all aspiring economists, are typically based on the assumption that natural resources are a given, inexhaustible, and efficiently exploited form of capital.

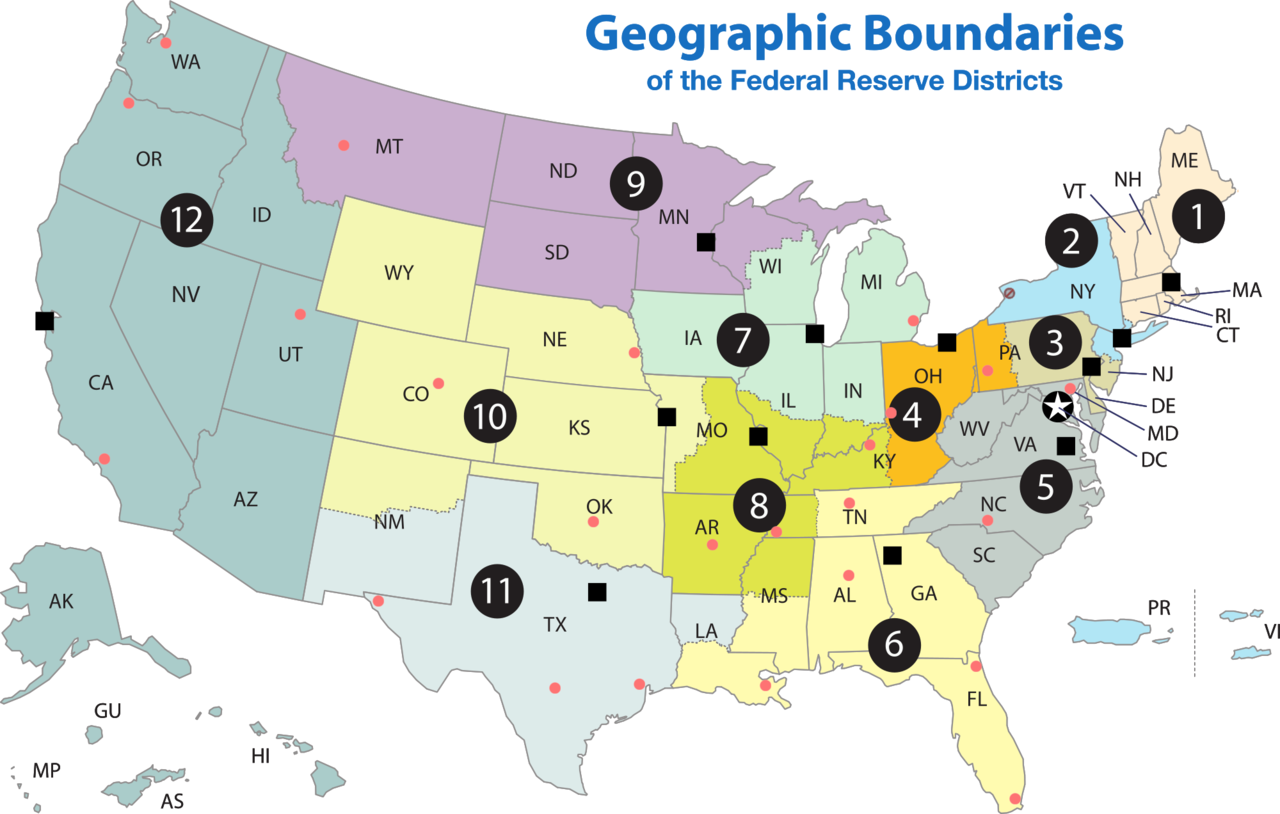

Federal Reserve Districts have a significant degree of bioregional coherence, increasing potential for big-picture, long-term capacity utilization assessments. (ChrisnHouston, CC BY-SA 3.0)

For estimating capacity utilization, then, the Fed focuses on the percentage of manufactured capital (plant and infrastructure) being used during the period in question. Their method entails simplistically “assuming sufficient availability of inputs to operate the capital in place.” They divide output (such as the latest year’s output of copper) by a “capacity index,” which seems to be nothing more than the output from a reference year, such as 2017.

Such an assumption belies the Fed’s notion of “sustainable maximum output.” It doesn’t take an overly long view to realize that “sustainable maximum output” is an oxymoron when applied to non-renewable resources such as oil and minerals. It should be plain as day that extracting and using non-renewable resources (such as combusting petroleum) constitutes an irreversible reduction of capacity.

And why doesn’t the Fed apply its capacity utilization concept, insufficient as it may be, to renewable natural resources such as timber, fisheries, and rangeland? At least with renewables, the concept of sustainable maximum output, or “maximum sustained yield,” is sound. Maybe the Fed ignores these resources because market share is below some unspecified threshold for the Fed’s consideration. The Fed might reason that it can’t cover all the bases of economic inputs, given its primary concerns over macroeconomic trends and policy.

Well, the Fed may want to consider that renewable natural resources comprise the foundation of the real economy. The economy has a trophic structure; a very basic principle of ecology with clear implications for monetary policy. The Fed should pay close attention to agricultural surplus, meaning production that feeds more than the farmer (as opposed to wasted excess production). It is the agricultural surplus that allows for a proportionate division of labor, which goes a long way toward determining a warranted money supply.

The Fed gets credit for recognizing the difference between actual and potential GDP. That clearly indicates some conceptual awareness of macroeconomic capacity. As usual, though, the ecological underpinnings of GDP are overlooked. From the supply side, it’s all about labor and capital. Alternatively, like at the Atlanta Fed, the difference between actual and potential GDP redounds to a Keynesian focus on demand.

Quantifiably Too Easy

A buildup to the Sustainable Monetary Policy Act can’t go without mentioning some highlights of the banking itself, as practiced or precipitated by the Fed while it endeavors to “maintain long run growth of the monetary and credit aggregates.” All that borrowing alluded to in the opening paragraph—borrowing conduced by lowering the federal funds rate—means the banking system must produce more money, far beyond the cumulative balances of their reserves.

When commercial banks issue loans, the money typically gets deposited, temporarily at least, at other banks, which are likely to loan some or all these new deposits, too. The “money multiplier” kicks in, “producing” multiples of the original amount of new (freshly loaned) money.

Before 2020, it was fashionable to calculate precisely how many dollars could be created in the century-old system of “fractional reserve banking.” For example, with a million dollars of deposits and a reserve requirement of 10%, nine million dollars of new money (minus some change) could be created.

On March 15, 2020, the Federal Reserve System abolished fractional reserve requirements and adopted a more subjective (and more opaque) “ample reserves” regime. The consensus seems to be that “ample” would be a more fitting adjective for “liquidity” than “reserves” under this new regime. To put it in lay terms, money got looser yet.

Much of the fiat money created by banks turns “fictional,” wound up in assets far removed from the real economy. (vonmeer, CC BY-NC-ND 3.0)

Beyond reserve considerations, the Fed can simply computerize new money into existence. Perhaps the most infamous episode was the “quantitative easing” (QE) following the 2008 financial crisis and commencing in 2009, when the Fed “purchased” $1.25 trillion of mortgage-backed securities from imperiled commercial banks. It kept the financial system afloat, and how.

“Purchase” is a peculiar way to put it, considering the money didn’t come from a pre-existing supply, loaned in a free money market. Rather, the QE money was imagined mentally, decided upon politically, and manifested unto the balance sheets of commercial banks—the big ones like Goldman Sachs, Citibank, and Bank of America—at the touch of a keyboard.

A more socially acceptable episode of QE was when the Fed “purchased” $4.6 trillion of Treasury securities (bills, notes, and bonds) and agency mortgage-backed securities during the covid pandemic. The Fed pulled out all the stops to obviate the freezing of markets, prevent a liquidity crisis, and generally stabilize the financial system.

While these were exceptional episodes, a fear is spreading that QE has become a way of life in an increasingly indebted, unstable, and unsustainable economy. These hasty episodes of flooding the markets with money, whether producers are ready for it or not, have the “allocative effects” of enriching Wall Street investors instead. This phenomenon explains, to a large extent, the development of the “K-shaped economy,” with the rich getting richer—way richer, way faster—while the middle class heads toward poverty.

Meanwhile, as best we can tell, the Fed continues to ignore the ecological fundamentals behind the instability.

Political Viability and Statutory Context

Presumably no one is naïve enough to think that a Sustainable Monetary Policy Act, with features described or alluded to above, is politically viable at this point in history. On the other hand, to think such a policy will never be viable is hardly credible either. Governmental paradigm shifts with broad public appeal happen with some regularity. Think for example of Reinventing Government and the Contract with America, two substantive, policy-wonkish and legislatively laden movements in one decade (1990s).

Robert F. Kennedy delivered a famous critique of GDP growth at the University of Kansas. Will it be echoed at the Fed? (Bill Eppridge, CC BY-NC-SA 4.0)

Steady staters have two giant allies in the struggle for steady-state politics: sound science and common sense. Limits to growth get more obvious by the year. Meanwhile, scientists and ecological economists are painstakingly documenting the evidence. At some point, conventional economists and lawyers will see the writing on the wall.

Unprecedented policy stands a better chance—on Capitol Hill, in the White House, and at the Fed—if the policy itself is ready and waiting in legislative form. Prior to that, talk about policy reform is just that: talk. And with limits to growth, it’s not particularly uplifting or unifying talk, as it usually tends toward lament, warning, regret, finger-pointing and the like.

So, it’s time to go beyond mere talk and consider a first-cut Sustainable Monetary Policy Act (SMPA). It’s a proactive, positive vision that should resonate not only with steady staters, but with citizens concerned with a fair shake for all, stable money, and accountability at the Fed and through the banking system at large.

To make perfect sense of the SMPA as introduced below, readers must view it as a component of the Steady State Economy Act, which is intended as a self-sufficient, omnibus bill to move the country toward a steady state economy. With plenty of effort, a little bit of luck, and maybe divine providence, the Steady State Economy Act will catch a foothold on Capitol Hill during the 2030s.

Meanwhile, “feeder bills” may be proffered on an as-viable basis. With that approach, a standalone SMPA would probably find traction toward the end of the run, complementing especially the fiscal policy measures packaged in the Steady State Economy Act, including the Sustainable Budgets Act and the Sustainable Taxes Act.

The Act

The full title of the SMPA is “An Act to establish sustainable monetary policy conducive to and corresponding with sustainable real economic activity.” Section 1 provides the short title (Sustainable Monetary Policy Act).

A Federal Reserve System attuned to uneconomic growth would be a giant leap for mankind. (CASSE)

Section 2 comprises the findings and declarations of Congress. For paradigm-shifting legislation like the SMPA, Section 2 could very well be the most important one. It’s where the new paradigm is summarized. In Subsection (a)(3), for example, Congress finds that “The best available science indicates that the national and global economies are operating at or beyond their long-term environmental capacity, and therefore unsustainably.” That will clearly be a first in monetary legislation. The corresponding declaration is in Subsection (b)(5), “The Federal Reserve System must take every precaution to avoid the growth of the economy to a level that damages long-term ecological capacity.” (These clauses give rise to Sections 7-9 pertaining to the monitoring of ecological and economic capacity.)

Herald readers familiar with the trophic theory of money will find familiarity in Section 2(a)(12), where Congress finds that “a viable money supply with real purchasing power is ultimately dependent upon the agricultural surplus at the base of the economy, which allows for a division of labor and makes money a meaningful concept.” This is the basis for several mandates to follow.

Section 3 provides definitions, some of which will likely be firsts for statutory law, including “fund-service resources.” Among the many examples of fund-service resources, forests not only provide timber (stock-flow resources) but concurrently function as funds of carbon sequestration and pollination services. These economically crucial services appear to be entirely overlooked by the pre-SMPA Fed. This is a significant problem, because overlooking the value of fund-service resources is conducive to the drawdown or liquidation of natural capital stocks.

Section 4 is where the real action begins to manifest. It calls for reorganization, putting an end to the esoteric, “quasi-governmental” stature of the Fed, placing it squarely into the U.S. government as a cabinet-level agency, with the Fed Chair reporting directly to the President. This alone would engender substantial political support.

Readers will rightfully wonder, “How’s that going to look with a President like the growth-obsessed Donald Trump?” (Kevin Warsh would wonder, too.) Recall the assumption that the SMPA presupposes the broader SSEA, which mandates the Administration to engender a public-private transition to a steady state economy. Stemming from the SSEA, steady-state fiscal and regulatory policies are concurrently at play, making it far easier for the Fed to get in the steady-state game and stick with the program.

Conversely, having the Fed chair on the Cabinet, mandated toward the steady state economy, would provide for expert macroeconomic reinforcement, helping to hold presidents and Treasury secretaries accountable.

There’s more to Section 4, like positioning the Chairman of the Commission on Economic Sustainability (a SSEA construct) on the Fed’s Board of Governors, ex officio, to provide expert advice on ecological capacity. Similarly, it adds the President of the Federal Reserve Bank of Kansas City as an ex officio member of the Federal Open Market Committee (the body that sets the federal funds rate target), “for purposes of providing continual expertise on agricultural production.” Despite the general shake-up, Section 4 is designed to retain nearly all Fed board and staff, while adhering to the SSEA principle of “no net gain in bureaucracy.”

Section 5 is perhaps the most crucial section, next to the findings and declarations. Short and simple, it reorients the Fed with the new mandate of transitioning toward a steady state economy. It also calls for maintenance of a money supply “that reflects, waxes and wanes with the level of real economic activity,” fairly ensuring that at least this one effective way of keeping inflation at bay returns to Fed operations. Section 5 essentially precludes quantitative easing (short of a declaration of crisis by the Monetary Emergency Committee established in Section 14).

Section 6 calls for long-term planning; very long compared to what the Fed is accustomed to. As with the broader SSEA, Section 6 establishes a planning horizon of 150 years, essentially forcing the Fed to consider the natural world of environmental, ecological, meteorological, geological, and climatological forces. These are forces, ranging in predictability, that impact the real economy the Fed is called in Section 5 to dovetail the money supply with. Keeping these natural forces in mind will help prevent the Fed from reverting to the old mode of perpetual-growth thinking.

Section 7 establishes a Division of Ecological Capacity Monitoring to provide the Fed with expertise in natural capital accounting and the concepts and methods of ecological footprint and biocapacity assessment. This division will also provide educational resources to Fed Board and staff.

Section 8 kicks off a special role for the Federal Reserve Bank of Kansas City (home base of the aforementioned Tom Hoenig). Just as the New York Fed specializes in open market operations, and the Atlanta Fed specializes in payment systems, the Kansas City fed can and should—and in some ways has already started to—specialize in the agricultural surplus that literally and figuratively feeds the rest of the economy.

Section 9 helps the Fed bridge the gap from some of its old practices to the new. It builds upon the Fed’s economic “capacity utilization” assessment to a more ecologically valid approach. It expands the scope from short-term capital and labor capacity to long-term ecological and agricultural capacities.

Section 10 shifts the paradigm of the Fed from seeking zero gap between actual GDP and potential GDP. It should indeed close the gap, vis-à-vis employment, but not overall. The renewable natural resources at the trophic base of the economy need to thrive in a state of reasonable ecological integrity, and a gap between actual and potential GDP provides an insurance policy for natural disasters and geopolitical crises.

Section 11 addresses interest-rate management. While it eschews the details of open market operations, it echoes the goal of sustainability and indeed the steady state economy as populations stabilize. It reinforces the steady-state paradigm shift for the Board of Governors and the Federal Open Market Committee, and prohibits “incentivizing higher levels or faster rates of economic activity at any period during which the real economy is in ecological overshoot.”

Section 12 invokes (implicitly) the trophic theory of money and calls on the Fed to closely monitor food surpluses for more ecologically grounded insights to economic capacity and likewise to the scale of money supplies that will be neither inflationary nor deflationary.

Section 13 puts a cap on bank size and number, Section 14 limits quantitative easing to emergencies, and, as Congress runs out of gas for further monetary policy engineering, Section 15 requires the Fed to develop the detailed rules and regulations for achieving the goals and objectives of the Act (standard procedure for program-shifting legislation).

Monetary policy development has been a bridge too far for the sustainability sciences, and even in the ecological economics community. Let’s hope that the Sustainable Monetary Policy Act changes that. It could use some fleshing out over time, prior to the rollout of the omnibus Steady State Economy Act, but if we simply precipitated a paradigm shift in the Federal Reserve System—from growthmanship to steady statesmanship—the SMPA would be a profound success.

Brian Czech is CASSE’s Executive Director.

Brian Czech is CASSE’s Executive Director.

I think you’re right that at some primitive level, the leveling off of human population will get policymakers to entertain a more steady state world. For all sorts of reasons. I just hope it will happen before too many ecosystems have been pushed past their breaking point.

I recently watched ‘The Big Short’ and ‘Too Big To Fail’, both centered around the 2008 financial crisis, when the U.S. housing bubble burst, because of high-risk lending practices, specifically with sub-prime mortgages. Major financial institutions went bust and triggered a severe recession, with global repercussions.

Watching these movies gave me a short-lived sense of superiority, as if, somehow, I was privy to some insider information. In reality, I hardly understood many of the terms, but knew that what the suits were mumbling was of supreme importance to every American citizen. I was left with more questions than answers, though.

Asset-backed commercial paper (ABCP), Collateralized debt obligations (CDO), Shadow banking, Waterfall structure, Z score, haircut, CDO squared… anyone?

As a supporter of the CASSE agenda, I reveled in it all – the awful Wall Street folks (well, at least some of them) got their comeuppance – temporarily, as we now know. Good! Beyond that? It was all smoke and mirrors. I felt like the ant on a giant tire, relentlessly moving down, down, but not knowing why.

I know there are better-informed readers than I and many who understand all these financial terms. But do we all know HOW these terms come together via the Fed policy that clearly favors the financial economy, causing so much damage to the quality of our lives and those of future generations? In spite of the fact that we are witnessing, real-time, these resuscitating measures regularly now?

What was glaringly obvious was the chasm between the real economy and the financial economy. And this gap is what the deeply-researched Sustainable Monetary Policy Act (SMPA) addresses and endeavors to diminish, if not close it completely in future decades. Reading through it, I got the same feeling of the ant on the tire but moving UP, an expansive feeling, not a sinking one! (contd…)

This Act goes where few have gone before – painstakingly attempting to understand the obfuscatory language and Fedspeak which have become the norm. It is the first I have seen to address the real-financial gap, which is destroying our environment and maybe our species.

The current policy is also, sadly, accepted by almost all American citizens as “This is how ‘experts’ speak, and there’s no point even attempting to understand it; as long as I get my loan.” How many people have actually read through their financial loan documents? Or any investing document, instead of trusting a lender or financial advisor or friend, as the case may be? We accept that ‘good faith, the American way’ will carry us through; trust that the Fed will look out for us. Look where that attitude has landed us. Why? Because we don’t even read instruction manuals, let alone Fed policies. We have stopped questioning.

The SMPA does not cloak itself in obfuscation. Instead, it clearly points out that the base of our prosperity is agriculture and related assets. The language was not evasive or opaque. No ‘this is only for experts’ attitude. This Act is for every American citizen to read, understand and ask questions.

We have time to spend on the internet, watching movies, playing video games and spend hours on the screen. I decided to spend two hours, which I would have spent on mindless weekend browsing, to force myself to read this Act. Force, because our attention spans to anything more complicated than headlines, or maybe 1000-word articles, are miniscule.

We are already seeing the economy fray at the seams. The ‘only GDP growth matters’ argument is no longer working. Resuscitation attempts are getting more frequent. This Act gives us the weapons we need to question and suggest to those ‘experts’ – here is a different way to make this better. We can stand up to those ‘experts’ who speak in jargon and explain to them, in English, how we can create a sustainable economy for this country.